The Insurance Industry Just Got a Faster Path to Manage Its Own Risk. Your Denied Claim Still Waits in Line.

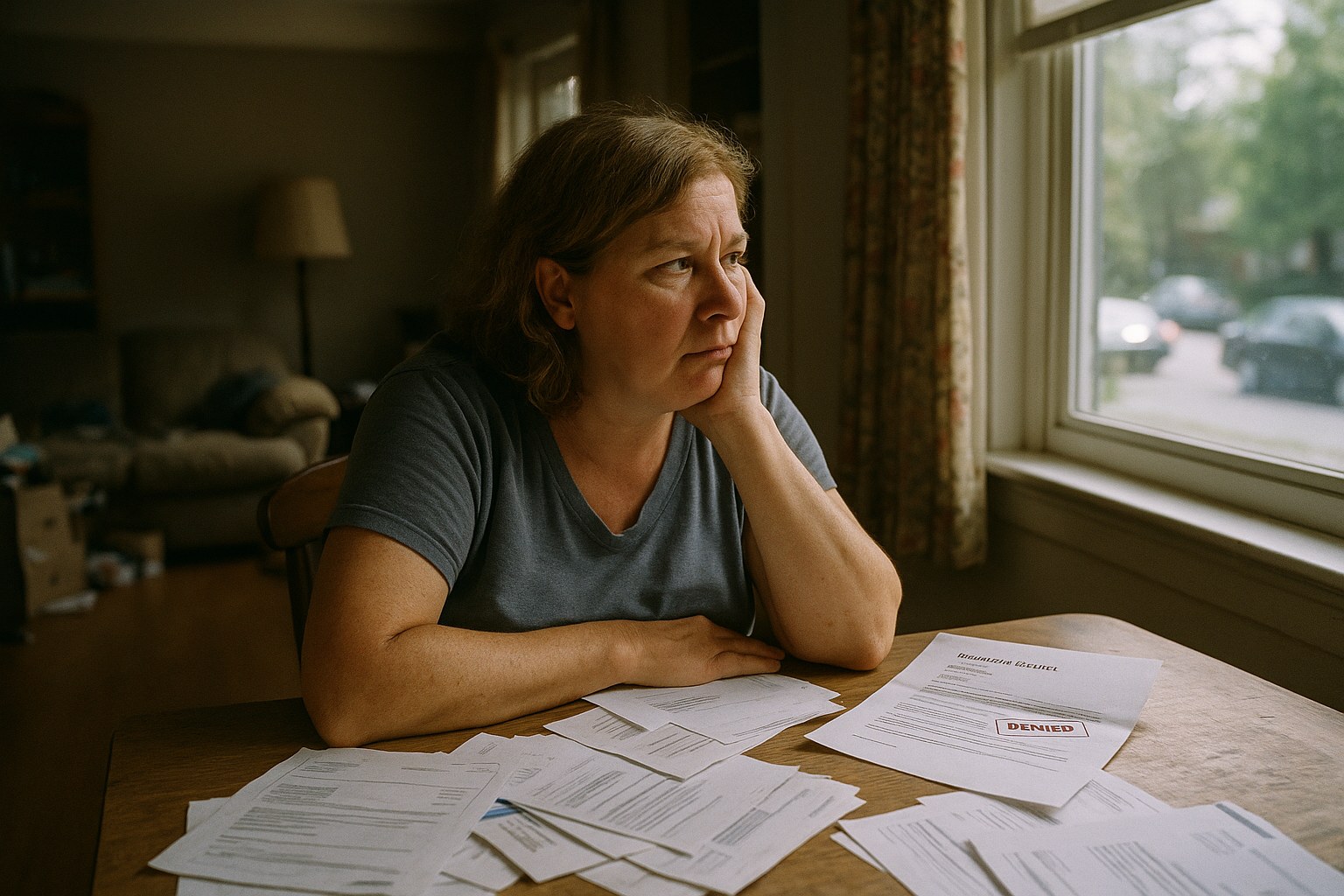

Picture two insurance claims moving through the system on the same day. One belongs to a multinational corporation setting up its own private insurer to co

7/15/2026 | 1 min read

See If You Have a Strong Insurance Claim

Take our 2-minute qualifier and find out if you're a strong candidate for representation — at no cost.

See If You Qualify — Free Eligibility Check →No fees unless we win · Takes under 2 minutes · No obligation

The Insurance Industry Just Got a Faster Path to Manage Its Own Risk. Your Denied Claim Still Waits in Line.

Picture two insurance claims moving through the system on the same day. One belongs to a multinational corporation setting up its own private insurer to cover its own risk. The other belongs to a Florida homeowner waiting on an adjuster to answer the phone about a leaking roof. Only one of those claims is getting a regulatory fast lane.

What happened

On July 14, 2026, the UK's two top insurance regulators, the Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA), laid out formal plans for what they're calling an "internationally competitive UK captive insurance regime," set to launch in 2027, according to Insurance Journal. A captive insurer is essentially a company that insures itself, or its corporate parent and affiliates, instead of buying coverage from an outside carrier.

The UK has historically lacked a tailored framework for these entities, which regulators say pushed many corporations to set up their captives overseas instead, in places like France and Italy, which opened the door to captives in 2023, and longtime captive-friendly domiciles like Ireland, Malta, Luxembourg, Sweden and Switzerland, the article reports. The government first announced its intent to fix that gap in July 2025, and regulators are now formally requesting industry input, with the consultation window closing October 14, 2026.

The proposal, for now limited to "single-parent" captives that insure only their own corporate group, has drawn enthusiastic reviews from the industry. PRA executive director David Bailey called it a plan that will "enhance the UK's competitive edge in insurance," per the same report. FCA deputy chief executive Sarah Pritchard framed it as a "pragmatic and proportionate" approach with "appropriate safeguards in place." Insurance broker Marsh called the proposal a "significant milestone," and Marsh Risk UK CEO James Addington Smith said the firm would spend the next three months helping "shape a framework that is proportionate, competitive and practical to implement." Stephen Cross of McGill and Partners went further, praising the plan for removing "the complex Solvency II reporting burden and risk margins" and setting up a "sensible four-to-six-week authorization process."

Why this matters to you

None of this happens in Florida, and none of it is a claim denial. But it's worth sitting with what regulators and the industry are actually excited about here: making it faster, cheaper, and less bureaucratically burdensome for large companies, insurers among them, to manage their own risk exposure on their own terms.

That's the energy the industry brings to the table when the subject is its own capital requirements, its own reporting obligations, its own authorization timelines. A four-to-six-week approval process. Lighter capital treatment. Fewer reporting hurdles. Brokers and captive managers spent years advocating for exactly this, and got regulators to listen.

Florida policyholders whose water-damage, hurricane, or liability claims sit unresolved for months don't have a trade association lobbying regulators on their behalf for a faster, lighter-touch process. There's no proposed regime promising a "four-to-six-week" turnaround on a delayed adjuster inspection or a denied estimate. The contrast isn't a coincidence, it's a reflection of where regulatory and industry attention actually goes: toward reducing friction for capital, not toward reducing the wait for the person holding the policy.

The bigger pattern

This is the part worth saying plainly: the insurance industry is very good at organizing itself to reduce its own burden, and comparatively uninterested in applying that same energy to reducing the burden it places on policyholders.

When it's insurers and their brokers asking for regulatory change, the request is specific, technical, and effective: proportionate capital treatment, streamlined authorization, less reporting overhead, as McGill's Stephen Cross laid out in describing exactly what "captive owners actually need," per Insurance Journal. Regulators respond with consultations, timelines, and named officials publicly committing to "pragmatic and proportionate" frameworks.

Compare that to how the claims process works for an ordinary policyholder. There's no comparable industry-wide push to shrink the time it takes to answer a claim, to explain a denial in plain language, or to pay an undisputed portion of a loss while a dispute over the rest continues. The asymmetry isn't an accident of history. It's what happens when one side of the relationship, the insurers and the brokers who serve them, has the lobbying infrastructure, the trade associations, and the regulatory relationships to get its priorities addressed quickly, while the other side, individual policyholders, has none of that and has to rely on the claims process working as promised or, when it doesn't, on litigation.

The captive regime itself isn't the villain here. Large companies managing their own risk more efficiently is a legitimate business goal. But it's a useful window into incentives: the industry mobilizes fast and effectively when the ask is "make our own risk management cheaper and faster." Florida homeowners and drivers waiting on a fair claims decision deserve to notice that the same urgency rarely shows up on their side of the ledger, and to ask why.

What people in this situation should know

If you're a Florida policyholder dealing with a slow-moving, underpaid, or denied claim, there are general things worth understanding, though nothing here is advice for your specific situation.

First, insurance is a contract, and the specific policy language, not general industry practice, controls what you're owed. Read your denial letter or lowball estimate closely and ask what basis the carrier cited.

Second, Florida policyholders generally have options when they disagree with how a claim was handled, which can include requesting appraisal, filing a complaint with state insurance regulators, or seeking a second opinion on the scope or value of damage. Depending on the facts, there may also be legal avenues to challenge how a claim was investigated or valued.

Third, documentation matters. Photos, repair estimates, communications with the carrier and adjuster notes can all become important if a dispute escalates.

Finally, time limits apply to insurance disputes, so if a claim has stalled or been denied, it's worth understanding your options sooner rather than later.

This article is general information about insurance industry trends and Florida policyholder rights. It is not legal advice and does not create an attorney-client relationship. Every policy and claim is different. If you're dealing with a denied, delayed, or underpaid insurance claim in Florida, you may want to have the specific facts of your situation reviewed by a licensed attorney.

If you're navigating a disputed property or insurance claim in Florida, a consultation with Louis Law Group may help you understand what options could be available given the specifics of your policy and claim.

Sources

Is your insurance company handling your claim fairly?

Answer 5 questions. We'll analyze your claim against Florida property insurance law and show you exactly where you stand.

General information only, not legal advice. Based on Florida insurance law and claim best practices.

Get Your Free Property Damage Checklist

24-step claim guide — protect your rights after damage to your home

Free. No spam. Unsubscribe anytime.

Find Out If You Qualify — Free Case Review

No fees unless we win · 100% confidential · Same-day response

★★★★★ 4.7 · 67 Google Reviews

What Our Clients Say

Real reviews from real clients who fought their insurance companies — and won.

"Citizens denied our roof leak claim, but this firm fought for us and got money for our repairs. We even had funds left over after fixing the roof."

"Pierre and his team are amazing. They truly cater to their clients and help you get the most from your insurance company."

"When my insurance company denied my roof damage claim, Louis Law Group stepped in and fought for me. I'm extremely satisfied with the results they obtained."

"They accomplished exactly what they set out to do and helped me finally receive my insurance check."

"Louis Law Group handled our homeowners insurance dispute and got results much faster than we expected. Excellent service and great communication."

"Very professional attorneys with outstanding attention to detail. They will not stop fighting for their clients."

* Reviews from Google. Results may vary by case.

How it Works

No Win, No Fee

We like to simplify our intake process. From submitting your claim to finalizing your case, our streamlined approach ensures a hassle-free experience. Our legal team is dedicated to making this process as efficient and straightforward as possible.

You can expect transparent communication, prompt updates, and a commitment to achieving the best possible outcome for your case.

Free Case EvaluationLet's get in touch

We like to simplify our intake process. From submitting your claim to finalizing your case, our streamlined approach ensures a hassle-free experience. Our legal team is dedicated to making this process as efficient and straightforward as possible.

12 S.E. 7th Street, Suite 805, Fort Lauderdale, FL 33301