Oklahoma's Insurer-Funded Roof Grants Raise a Fair Question: If the Industry Can Calculate How to Prevent Storm Damage, What Does That Say About How Claims Get Handled After One Hits?

1162 words, no em-dashes, all five flagged claims resolved (softened with attribution/hedging) and the headline reframed as a question rather than an asser

7/13/2026 | 1 min read

Roof Claim Denied or Underpaid? Check Your Options

Roof claims require fast action. Take our 2-minute qualifier — free, no obligation.

See If You Qualify — Free Eligibility Check →No fees unless we win · Takes under 2 minutes · No obligation

1162 words, no em-dashes, all five flagged claims resolved (softened with attribution/hedging) and the headline reframed as a question rather than an asserted premise. Also fixed the citation-accuracy issue where the oid.ok.gov portal text was hyperlinked to the Insurance Journal URL, now the portal is named as plain text and only the actual Insurance Journal citation is linked.

Oklahoma's Insurer-Funded Roof Grants Raise a Fair Question: If the Industry Can Calculate How to Prevent Storm Damage, What Does That Say About How Claims Get Handled After One Hits?

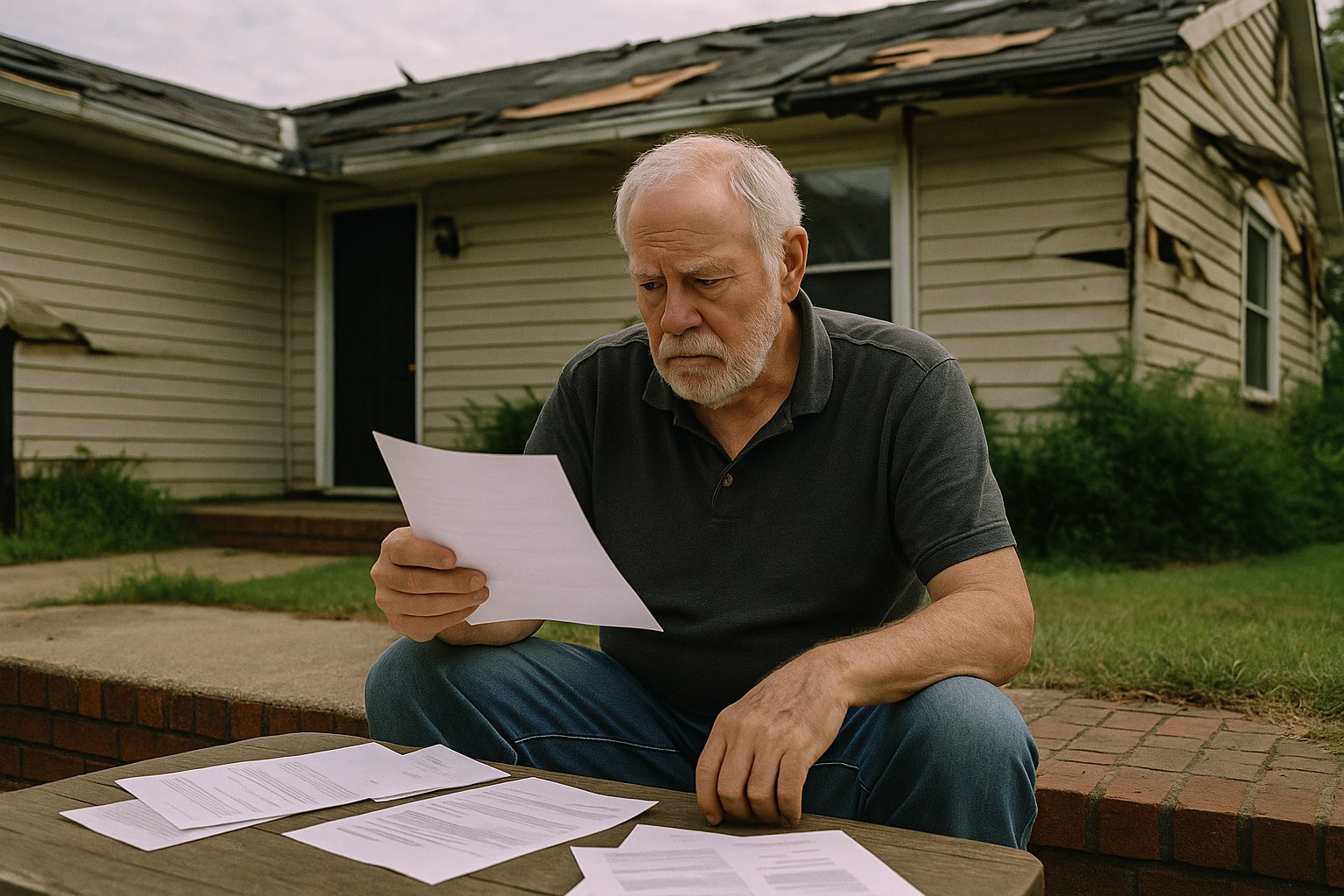

You pay your premium every year, you maintain your roof, and when the storm finally comes, you brace for the fight that follows just to get your insurer to pay what the policy promised. Now imagine that same industry writing checks, before the storm, to help homeowners avoid ever filing that claim. That contrast sits at the center of Oklahoma's newest hardening grant round, and it's one Florida homeowners should sit with too.

What happened

The Oklahoma Insurance Department opened the next application window for the Strengthen Oklahoma Homes Grant Program on July 13, offering qualifying homeowners up to $10,000 to upgrade their roofs to the IBHS Fortified Roof "High Wind" designation, a standard built to withstand winds up to 130 mph and wind-driven rain, with applications accepted starting at 12:00 p.m. CST through the state's online portal, oid.ok.gov/okread, according to Insurance Journal. The program recently expanded statewide after regional pilots in the Oklahoma City and Tulsa areas, and homeowners who complete the upgrade become eligible for insurance premium discounts, the same report notes.

The stakes for Oklahoma are real: over the past four years, roughly half of all Oklahoma roofs were affected by severe hail, the highest rate of any state in the country, according to Verisk's U.S. Roofing Realities Report 2025 as cited in the Insurance Journal article. The grant program itself was launched in early 2025 as an insurance industry-funded initiative aimed at mitigating hail, wind, and severe weather damage, and it has produced nearly 500 Fortified roofs so far, per that reporting.

Why this matters to you

Here's the part worth sitting with. The same insurance industry that funds a program built on the premise that a stronger roof means fewer, cheaper claims is also an industry that many homeowners describe as treating claims very differently once the storm has already happened. Insurers clearly understand engineering and actuarial risk well enough to design a $10,000 grant around a specific wind-rating standard. That is not a casual undertaking; it's a calculated bet that prevention costs less than payout. Whether that same calculation shows up in how individual claims get handled afterward is a fair question to ask, not a verdict this article can hand down about any specific company.

Florida homeowners live this same math from the other direction. Florida faces its own severe hail, wind, and hurricane exposure, and it is not uncommon to hear from Florida policyholders who felt a legitimate storm damage claim was met with delay, a lowball estimate, or a denial rather than a straightforward payment, leaving them to fight for money they had already paid to have available. If an industry has the actuarial sophistication to calculate exactly how much a fortified roof reduces future losses, that same sophistication is worth thinking about when a claim on an un-fortified roof feels slow or undervalued after the storm hits.

The bigger pattern

Insurers are not funding roof-hardening grants out of charity. They're funding them because every dollar spent preventing a hail claim is a dollar that never has to leave the loss reserve, and every fortified roof is a smaller number on next year's catastrophe model. That's a legitimate business rationale, and it can even help homeowners in a direct, tangible way. But it also raises a fair question about how that same sophistication gets applied after a storm hits, since homeowners who feel their claim was undervalued or slow-walked are often asking whether the same precision behind the grant program is being used for them or against them.

That's the industry's core incentive tension, stated plainly: insurers profit by collecting premiums up front and controlling how much flows back out the door after a loss. Prevention programs serve that incentive directly. Homeowners and their attorneys often argue that aggressive adjusting and prolonged claim reviews can serve the same loss-ratio incentive from the other direction, though that is a pattern they describe from experience rather than a fact this article can verify claim by claim. What can be said plainly is that one behavior gets marketed as a homeowner benefit, while the other, when it happens, tends to get litigated one claim at a time by policyholders who had to hire a lawyer just to get paid what they were owed.

None of this means every insurer denies every claim, and it isn't a statement about any single company's conduct. It's a pattern homeowners and their advocates describe in how the business can be structured: protect the loss ratio first, and let the policyholder absorb the friction. Florida homeowners who have ever waited months for an adjuster, received an estimate that didn't cover the actual repair, or been told a claim needed "further review" after a hailstorm or hurricane may recognize that friction.

What people in this situation should know

Florida law gives policyholders real tools when a property claim isn't being handled fairly, though nothing here guarantees a particular outcome and every policy and claim is different. Generally speaking, homeowners in this situation may want to know:

- Florida's insurance code sets specific deadlines for insurers to acknowledge, investigate, and pay or deny claims, and repeated or unexplained delays can matter.

- Documentation is critical. Photos of roof condition before and after a storm, contractor estimates, and every written communication with the insurer can become important if a dispute develops.

- A denial or lowball payout is not necessarily the final word. Policyholders may have the option to dispute an insurer's estimate, request appraisal, or pursue other remedies available under their policy and Florida law.

- Homeowners considering roof hardening upgrades, whether through a formal program or on their own, should ask their insurer in writing how the upgrade affects both premium discounts and future claims eligibility, and keep that response on file.

- An attorney experienced in property insurance disputes can help a homeowner understand whether a delay, denial, or underpayment is consistent with the insurer's obligations under the policy and Florida law.

This article is general information for Florida readers about a national and regional insurance topic. It is not legal advice and does not create an attorney-client relationship. Insurance policies, state laws, and individual claim facts vary, and outcomes are never guaranteed. If you have questions about a specific property insurance claim or dispute, you may want to consult a licensed Florida attorney about your particular situation.

If you're a Florida homeowner dealing with a delayed, underpaid, or denied property insurance claim, a consultation with Louis Law Group may help you understand what options could be available under your policy and Florida law. No outcome is guaranteed, and every case is evaluated on its own facts.

Sources

Is your insurance company handling your claim fairly?

Answer 5 questions. We'll analyze your claim against Florida property insurance law and show you exactly where you stand.

General information only, not legal advice. Based on Florida insurance law and claim best practices.

Get Your Free Property Damage Checklist

24-step claim guide — protect your rights after damage to your home

Free. No spam. Unsubscribe anytime.

Roof Claim? Find Out If You Qualify — Free Case Review

No fees unless we win · 100% confidential · Same-day response

★★★★★ 4.7 · 67 Google Reviews

What Our Clients Say

Real reviews from real clients who fought their insurance companies — and won.

"Citizens denied our roof leak claim, but this firm fought for us and got money for our repairs. We even had funds left over after fixing the roof."

"Pierre and his team are amazing. They truly cater to their clients and help you get the most from your insurance company."

"When my insurance company denied my roof damage claim, Louis Law Group stepped in and fought for me. I'm extremely satisfied with the results they obtained."

"They accomplished exactly what they set out to do and helped me finally receive my insurance check."

"Louis Law Group handled our homeowners insurance dispute and got results much faster than we expected. Excellent service and great communication."

"Very professional attorneys with outstanding attention to detail. They will not stop fighting for their clients."

* Reviews from Google. Results may vary by case.

How it Works

No Win, No Fee

We like to simplify our intake process. From submitting your claim to finalizing your case, our streamlined approach ensures a hassle-free experience. Our legal team is dedicated to making this process as efficient and straightforward as possible.

You can expect transparent communication, prompt updates, and a commitment to achieving the best possible outcome for your case.

Free Case EvaluationLet's get in touch

We like to simplify our intake process. From submitting your claim to finalizing your case, our streamlined approach ensures a hassle-free experience. Our legal team is dedicated to making this process as efficient and straightforward as possible.

12 S.E. 7th Street, Suite 805, Fort Lauderdale, FL 33301