Insurers Are Racing to Build AI Armies. The Real Question Is What They're Building Them For.

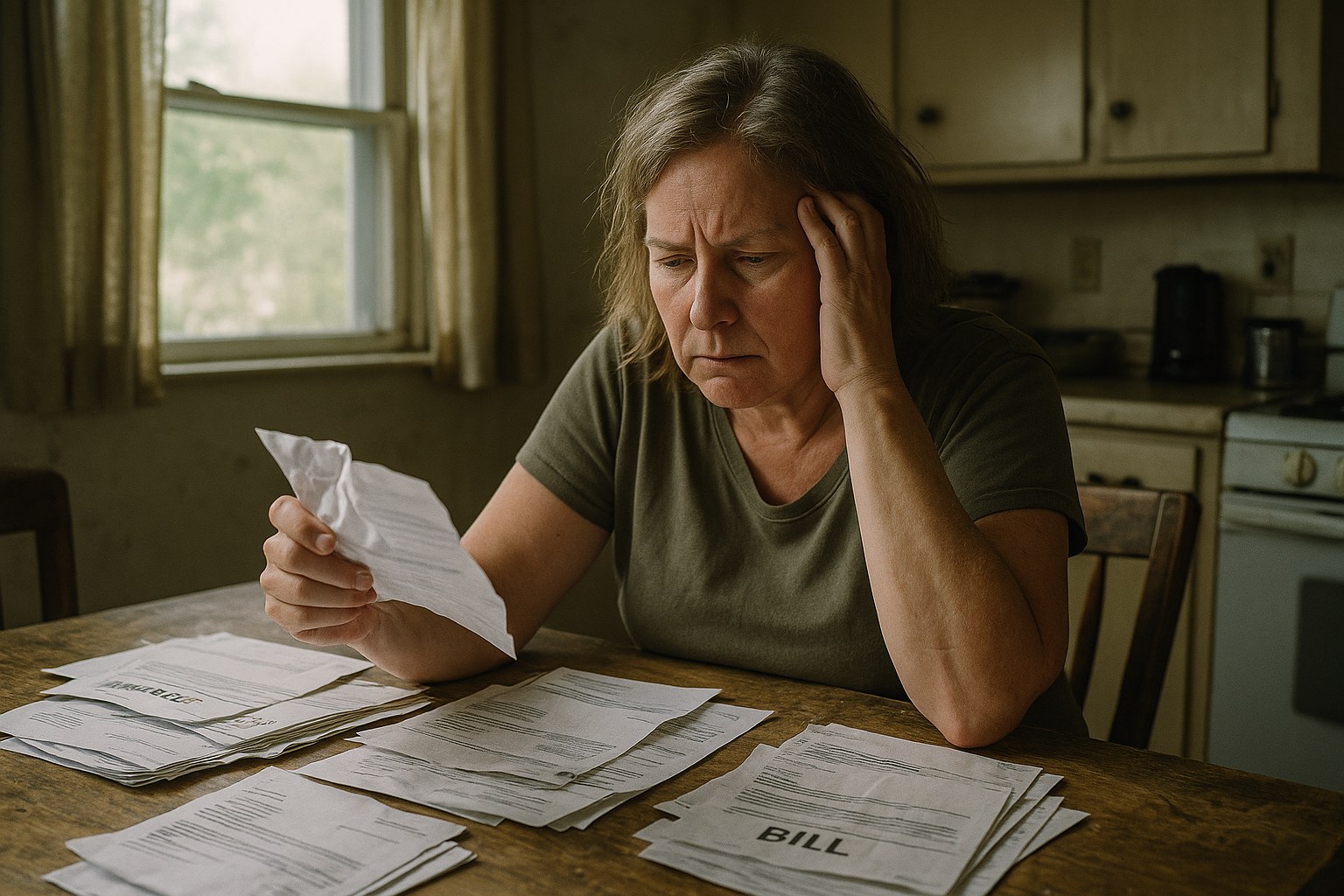

You file a claim after a storm, a wreck, or a denied treatment, and the response that comes back reads like it was written by nobody in particular. No adju

7/13/2026 | 1 min read

See If You Have a Strong Insurance Claim

Take our 2-minute qualifier and find out if you're a strong candidate for representation — at no cost.

See If You Qualify — Free Eligibility Check →No fees unless we win · Takes under 2 minutes · No obligation

Insurers Are Racing to Build AI Armies. The Real Question Is What They're Building Them For.

You file a claim after a storm, a wreck, or a denied treatment, and the response that comes back reads like it was written by nobody in particular. No adjuster's judgment, no context, just a number. If that has ever happened to you, a new industry ranking on insurer AI investment should make you pay closer attention, not less.

What happened

A London-based benchmarking firm called Evident has published its second annual ranking of AI "maturity" among 30 of the world's largest insurance and reinsurance companies, and the numbers show an industry moving fast. According to the analysis, one out of every 50 employees across these 30 carriers is now classified as an AI specialist, and across the group, AI-specialist roles expanded 32% over the past year even as overall insurer employment declined slightly, Insurance Journal reports.

Evident ranked Allianz as the top overall AI maturity leader this year, unseating AXA, which held the top spot last year. Allianz also leads on the "Talent" pillar, the single largest factor in Evident's scoring at 45% of the total index, with 28% more AI professionals in its workforce than AXA, per the report cited by Insurance Journal. Chubb climbed from eighth to third place in talent rankings year over year, and USAA, last year's talent leader, dropped to fourth after ranking near the bottom on "talent development" despite still leading on raw talent capability, according to the same reporting. The report also found that 11 of the 30 insurers analyzed now have a Chief AI Officer or equivalent senior role, and two-thirds of those executives have held the position for less than a year, Insurance Journal notes.

Why this matters to you

None of this is a hidden or theoretical trend. It is a public, industry-published scoreboard of how aggressively the largest insurance companies are building automated decision-making capacity, measured in headcount, leadership structure, and development programs. Evident's report measures talent and maturity, not where specific AI systems are deployed, so it does not tell us which parts of the claims process any given carrier has automated. Still, for a Florida policyholder it is reasonable to ask the question, because insurers broadly have been extending AI into claims-related work in recent years, and a workforce this heavily staffed with AI specialists could plausibly be building toward any part of that pipeline: intake, damage estimation, medical necessity review, fraud flagging, or settlement calculation. That is a plausible inference about the direction of investment, not a finding in the report about what any named carrier's systems currently do.

Across these 30 insurers, AI-specialist roles grew 32% in a year while overall headcount at those same companies slipped slightly, as the Evident data shows. That is an industry-wide pattern, not a single company's growth rate, but it still tells you where the industry's institutional energy is going as a whole. That does not automatically mean your next claim decision was generated by an algorithm instead of a person who read your file. It does suggest that the industry's investment in that direction is accelerating, at a pace the industry itself is now publishing in a competitive ranking. If you are a policyholder in Florida who has ever felt like a claim denial or lowball offer arrived too fast, too generic, or too disconnected from the specifics of your loss, this ranking is a window into the infrastructure the industry is building, even if it cannot tell you exactly how any one insurer is using it.

The bigger pattern

Here is the uncomfortable question this ranking raises and does not answer: built to do what, exactly, and for whose benefit?

In our view, it is unlikely that insurers are staffing up on AI specialists, appointing Chief AI Officers, and competing publicly for "maturity" rankings primarily in order to pay more claims, faster, at higher amounts. A more plausible reading, and one this article argues rather than reports as established fact, is that AI investment is aimed at least in part at cutting costs and protecting loss ratios, the internal metric that shapes shareholder returns. An industry racing to build AI talent while overall headcount at these carriers shrinks slightly looks, on its face, like an industry optimizing for efficiency and margin. Whether that also serves the people paying premiums every month is a separate question this ranking does not answer.

That is an inference about incentive structure, not a factual finding about any named carrier's intent, and Evident's report does not measure intent either. Policyholder advocates and plaintiffs' attorneys have long described a pattern in claims handling that involves added review steps, denials of what can plausibly be denied, underpayment of what cannot be denied outright, and slow, expensive dispute processes for policyholders who object. Nothing in this ranking proves that any of the 30 companies studied engages in that pattern. But it is fair to ask whether faster, more automated systems make that kind of pattern, where it exists, easier to run at scale rather than harder, especially when the companies deploying these systems are, by their own account, focused on converting AI investment into performance. Chubb's chief executive, for instance, was described in Evident's report as explicit about the company's focus on "converting" its AI investment into results, according to Insurance Journal's coverage. Speed and consistency at scale are not automatically the same thing as fairness to an individual policyholder standing in front of a wrecked home or a denied medical claim, and nothing in this ranking suggests the industry is measuring itself on that basis at all.

What people in this situation should know

If you believe a claim was denied, delayed, or underpaid unfairly, whether or not automation played a role, Florida policyholders generally have options worth understanding, though none of them are guaranteed to change an outcome.

You typically have the right to request a written explanation for a denial or reduced payment, and to ask the insurer for the documentation, estimates, or reports that supported its decision. Many property policies include an appraisal process, a contractual mechanism for resolving disputes over the amount of a loss without going straight to litigation. Depending on the facts, some policyholders may also have grounds to explore a bad faith claim against an insurer that failed to handle a claim properly, though these cases turn heavily on specific conduct and timing.

Deadlines matter. Florida law imposes statutes of limitations and, for certain property claims, specific notice-of-claim windows, so waiting too long to act can foreclose options that might otherwise have been available. Keeping your own copies of communications, photos, estimates, and denial letters, and not accepting a first offer as final, are reasonable steps regardless of how a decision was reached.

This article is general information about a public industry report and does not constitute legal advice, and it does not evaluate the facts of any individual claim. Insurance policies, claim histories, and applicable law vary, and nothing here should be relied on as a substitute for individual legal counsel. If you believe your property or injury claim was mishandled, you may want to consult a Florida attorney to review your specific policy and circumstances before deciding how to proceed.

If a claim decision on your Florida property or injury case felt rushed, inconsistent, or hard to get a straight answer about, a consultation with Louis Law Group could help clarify what options, if any, may be available in your specific situation.

Sources

Is your insurance company handling your claim fairly?

Answer 5 questions. We'll analyze your claim against Florida property insurance law and show you exactly where you stand.

General information only, not legal advice. Based on Florida insurance law and claim best practices.

Get Your Free Property Damage Checklist

24-step claim guide — protect your rights after damage to your home

Free. No spam. Unsubscribe anytime.

Find Out If You Qualify — Free Case Review

No fees unless we win · 100% confidential · Same-day response

★★★★★ 4.7 · 67 Google Reviews

What Our Clients Say

Real reviews from real clients who fought their insurance companies — and won.

"Citizens denied our roof leak claim, but this firm fought for us and got money for our repairs. We even had funds left over after fixing the roof."

"Pierre and his team are amazing. They truly cater to their clients and help you get the most from your insurance company."

"When my insurance company denied my roof damage claim, Louis Law Group stepped in and fought for me. I'm extremely satisfied with the results they obtained."

"They accomplished exactly what they set out to do and helped me finally receive my insurance check."

"Louis Law Group handled our homeowners insurance dispute and got results much faster than we expected. Excellent service and great communication."

"Very professional attorneys with outstanding attention to detail. They will not stop fighting for their clients."

* Reviews from Google. Results may vary by case.

How it Works

No Win, No Fee

We like to simplify our intake process. From submitting your claim to finalizing your case, our streamlined approach ensures a hassle-free experience. Our legal team is dedicated to making this process as efficient and straightforward as possible.

You can expect transparent communication, prompt updates, and a commitment to achieving the best possible outcome for your case.

Free Case EvaluationLet's get in touch

We like to simplify our intake process. From submitting your claim to finalizing your case, our streamlined approach ensures a hassle-free experience. Our legal team is dedicated to making this process as efficient and straightforward as possible.

12 S.E. 7th Street, Suite 805, Fort Lauderdale, FL 33301