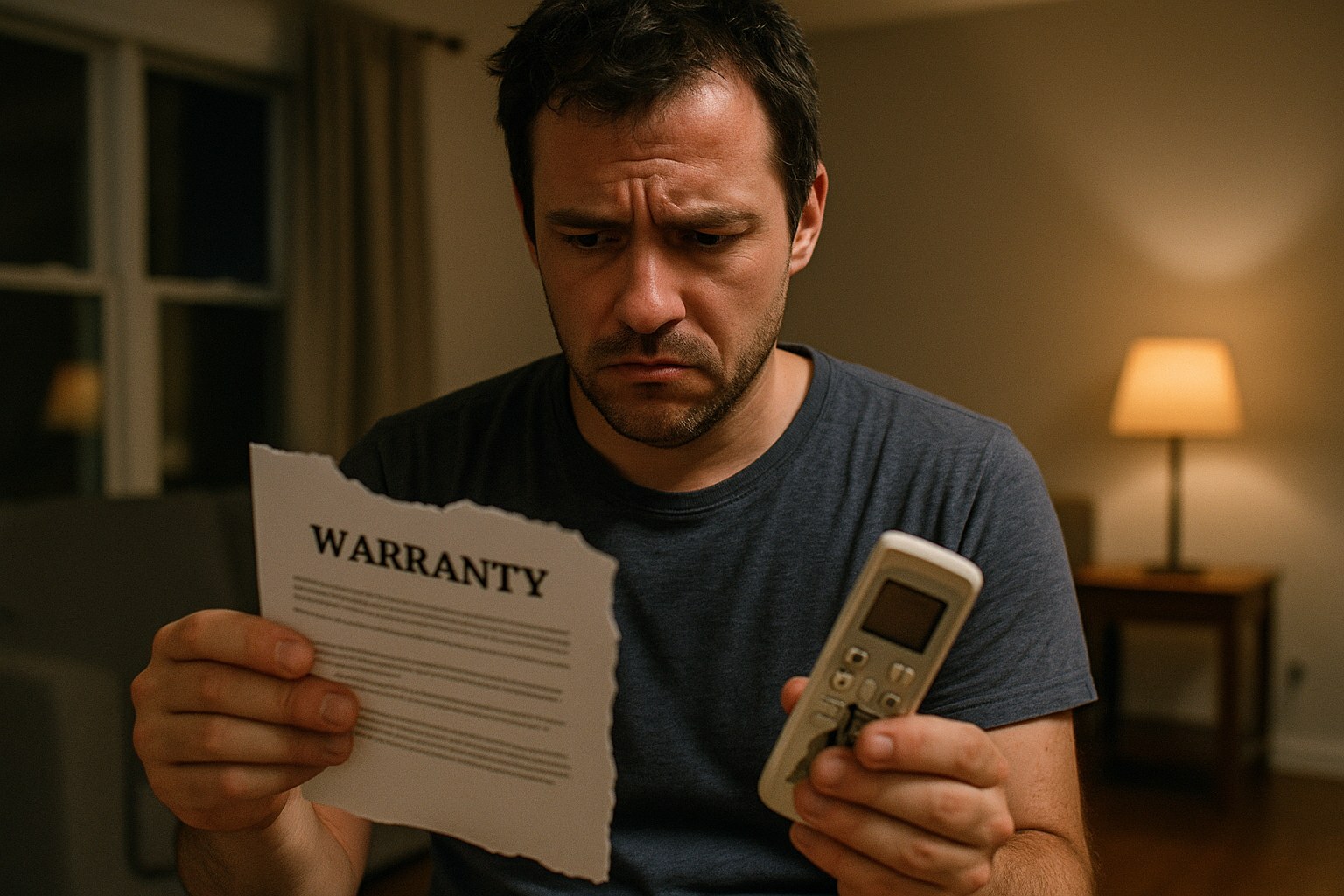

Forbes Ranked the "Best" Home Warranty Companies. It Didn't Rank How Often They Say No.

You pay the monthly premium on time, every month, for a home warranty or a vehicle service contract. Then the AC dies in August or the transmission goes on

7/3/2026 | 1 min read

Warranty Claim Denied? See If You Qualify

Take our 2-minute qualifier and find out if your denied warranty or service-contract claim qualifies for representation — at no cost.

See If You Qualify — Free Eligibility Check →No fees unless we win · Takes under 2 minutes · No obligation

Forbes Ranked the "Best" Home Warranty Companies. It Didn't Rank How Often They Say No.

You pay the monthly premium on time, every month, for a home warranty or a vehicle service contract. Then the AC dies in August or the transmission goes on the highway, and the company that took your money for years suddenly needs paperwork you never knew you had to keep. The "best of" lists rarely mention that part.

What happened

Forbes Advisor published its rankings of the best home warranty companies of 2026, following a familiar format of comparing pricing, coverage caps, and plan tiers across providers. CNBC Select runs a similar list, ranking the best home warranty companies of July 2026, and Reviews.com has its own comparison of top providers. These lists sit alongside the Better Business Bureau's own directory of home warranty plans and the complaint histories filed against them.

What none of these rankings measure directly is how often a claim gets denied once you actually need the coverage. That gap shows up elsewhere. A local news segment recently covered a lawsuit accusing a home warranty company of failing to fix a broken air conditioning system despite the homeowner paying for coverage. Other law firms have also published entire explainers asking "can I sue American Home Shield?" That kind of page does not establish anything about how any specific company actually handles claims. What it does show is that enough consumers apparently search that exact question for a law firm to think it is worth an entire page answering it.

None of this means every warranty company denies claims in bad faith, or that every ranked provider on Forbes' list operates the same way. It means the ranking criteria (price, plan variety, star reviews) and the lived experience of filing a claim are two different measurements, and consumers usually only discover which one matters when something breaks.

Why this matters to you

If you're a Florida homeowner, your AC unit isn't optional coverage, it's survival equipment for half the year. If you're a Florida driver, your car isn't optional either; you likely need it to get to work, to a doctor, to pick up your kids. Home warranties and vehicle service contracts get marketed the same way: pay a flat monthly fee, and stop worrying about the big repair bill.

But the value of that promise depends entirely on what happens the day you file a claim. Was the compressor failure caused by "lack of maintenance" you can't prove you performed? Was the transmission issue linked to a "pre-existing condition" that supposedly predates your contract, even though the car ran fine the day before? These are the exact junctures where a warranty holder finds out whether they bought protection or a subscription to paperwork.

Florida homeowners and drivers who are paying monthly for this kind of protection deserve to know, before something breaks, what the actual denial experience looks like, not just where a company lands on a rankings page.

The bigger pattern

Here is the opinion part, and it's not really about any one company on any list. It's about an entire product category built on a predictable structure.

Home warranty contracts and vehicle service contracts are cousins. Both are sold as peace of mind. Both are stuffed with exclusions that only become relevant, and only get read closely, at the exact moment a customer files a claim. And both product categories, in our view, tend to lean on the same handful of levers when a claim is expensive: call it a pre-existing condition, call it a maintenance failure, or call it outside the definition of covered "mechanical breakdown."

The vehicle service contract industry generally, monthly "bumper-to-bumper" coverage plans marketed to drivers, runs on a similar logic. The pitch is simple and reassuring. In our assessment, the claims process is often where the fine print does its work: a "required maintenance" record a customer can't produce years later, a technicality about which specific part failed, a definitional argument over what counts as a covered powertrain component versus ordinary wear. The incentive structure, as we see it, practically writes itself. A dollar not paid out on a claim is a dollar of margin, and a contract with enough exclusions can give an administrator a plausible basis to decline a given claim.

That is the pattern worth naming, not any single company's guilt, but the business model itself as we understand it: sell broad-sounding coverage, price it low enough to move volume, and lean on fine-print definitions to manage the loss ratio. Home warranty companies that advertise "whole home coverage" and then dispute a claim as a pre-existing condition would, in our view, be running a comparable playbook with different appliances. A consumer who paid faithfully for eighteen months and then gets a denial letter on month nineteen isn't necessarily unlucky. They may have run into the model working as designed, though every contract and every denial turns on its own facts.

What people in this situation should know

If you've had a home warranty or vehicle service contract claim denied, a few things are generally worth knowing under Florida law, without any guarantee about how your specific situation will turn out:

- Get the denial in writing, with the stated reason. A verbal "it's not covered" from a call center is not the same as a documented denial reason, and you'll want that reason on paper if you dispute it.

- Keep every maintenance and repair record you have, even informal ones like receipts or texts to a mechanic or technician, since "lack of maintenance" denials often hinge on exactly this kind of documentation.

- Read the actual contract, not the marketing page, for how the company defines "pre-existing condition," "mechanical breakdown," and "required maintenance." These definitions, not the sales pitch, control the claim.

- Understand that a denial is not always the final word. Depending on the contract terms and the facts, consumers may have options ranging from an internal appeal to a breach of contract claim, and in some circumstances Florida consumer protection statutes may be relevant.

- A pattern of denials across many customers is different from one disputed claim. Complaint histories, like those tracked by the Better Business Bureau, can be a useful data point when deciding how seriously to take a company's marketing claims.

This article is general information about industry practices and consumer rights, not legal advice, and it does not evaluate the specific facts of any individual's contract or claim. If you're dealing with a denied home warranty or vehicle service contract claim, the terms of your specific contract and the facts of your situation will determine what options may be available to you.

If you believe your vehicle service contract or home warranty claim was wrongly denied, it may be worth having a Florida attorney review your contract and the denial letter to see whether you have options worth pursuing. Louis Law Group offers consultations for Florida consumers who want to understand what those options might look like in their situation.

Sources

- Best Home Warranty Companies Of 2026 - Forbes Advisor

- Best Home Warranty Companies of July 2026 - CNBC Select

- Best Home Warranty Companies of 2025 - Reviews.com

- Home Warranty Plans Near Me - Better Business Bureau

- Lawsuit accuses home warranty company of not fixing AC

- Can I sue American Home Shield? - Kneupper & Covey

Find Out If You Qualify — Free Case Review

No fees unless we win · 100% confidential · Same-day response

★★★★★ 4.7 · 67 Google Reviews

What Our Clients Say

Real reviews from real clients who fought their insurance companies — and won.

"Citizens denied our roof leak claim, but this firm fought for us and got money for our repairs. We even had funds left over after fixing the roof."

"Pierre and his team are amazing. They truly cater to their clients and help you get the most from your insurance company."

"When my insurance company denied my roof damage claim, Louis Law Group stepped in and fought for me. I'm extremely satisfied with the results they obtained."

"They accomplished exactly what they set out to do and helped me finally receive my insurance check."

"Louis Law Group handled our homeowners insurance dispute and got results much faster than we expected. Excellent service and great communication."

"Very professional attorneys with outstanding attention to detail. They will not stop fighting for their clients."

* Reviews from Google. Results may vary by case.

How it Works

No Win, No Fee

We like to simplify our intake process. From submitting your claim to finalizing your case, our streamlined approach ensures a hassle-free experience. Our legal team is dedicated to making this process as efficient and straightforward as possible.

You can expect transparent communication, prompt updates, and a commitment to achieving the best possible outcome for your case.

Free Case EvaluationLet's get in touch

We like to simplify our intake process. From submitting your claim to finalizing your case, our streamlined approach ensures a hassle-free experience. Our legal team is dedicated to making this process as efficient and straightforward as possible.

12 S.E. 7th Street, Suite 805, Fort Lauderdale, FL 33301